Based on the previous article about the trap of the mortgage grace period, there are a lot of great experts who speak clearly and logically, as if it is the right thing to follow him, but they ignore that their own opinions are full of fallacies.

When buying a house is in the middle and late stages, after signing the contract, in addition to the loan application amount, the first and last payments, deed tax and performance fees have all been settled, and then you have to prepare to get the mortgage underwriting with the bank.

When applying for mortgage underwriting, there will be two options for you as a subsequent payment method. It seems that if you don’t write out this multiple-choice question and let some people who tell all kinds of fallacies read it carefully, I am really afraid that they will harm those around you. people.

There are two types of loan repayments to choose from, namely "average principal and interest amortization" and "average principal and interest amortization".

Average amortization of principal and interest: average monthly amortization of principal and interest

The total monthly payment of interest and principal is fixed, which is also the most common repayment method for ordinary people.

The main "advantage" is that the monthly payment amount is the same, making it easier to plan cash flow; however, the "disadvantage" is that the total interest expense is higher, and it is also the default mortgage repayment method of most banks.

Average interest amortization on principal: average monthly amortization of principal plus decreasing interest.

The principal repaid each month remains unchanged, but the interest is calculated based on the principal balance. Therefore, as more and more principal is repaid, the interest payable will decrease every month, causing the repayment amount to decrease monthly. It’s a repayment method that takes pains first and then gets sweetness later.

Since the initial monthly payment for principal amortization is relatively high, it is more recommended for those who rarely manage money and who often become a paycheck to paycheck at the end of the month, as it can be used as a passive savings.

The repayment methods of the two are different, but the most important difference is the overall amount of interest paid.

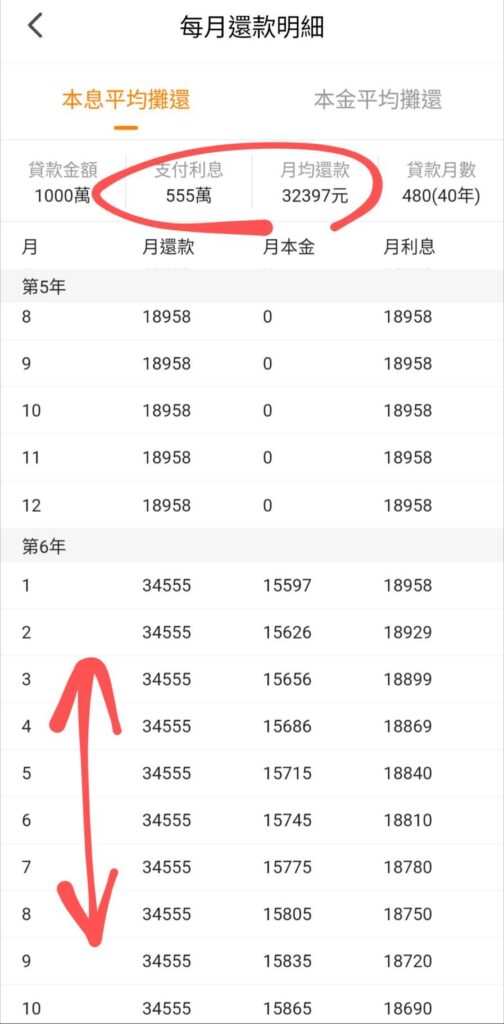

Take the Xinqing'an house purchase loan as an example. If all the conditions are met, the loan is 10 million, the grace period is five years, and it is extended for 40 years. The interest rate for the first two years is 1.775%, and the interest rate for the next 38 years is 2.275%. Leaving aside the sale , refinancing and early repayment problems, and the calculation is based on the payment period of the same bank.

Average amortization of principal and interest: average monthly repayment is 32,397 yuan, and total interest paid is 5.55 million.

Average principal amortization: first month repayment is 42,768 yuan, decreasing by 45 yuan every month, total interest paid is 5.03 million.

Does this seem clearer? The difference is that the "average amortization of principal and interest" has a monthly decreasing amount. If you pay off the loan over the full term, you will save a total of 520,000 less than the "average amortization of principal and interest". interest money.

Usually the bank will only show it to you. Of course, the interest rate allows them to receive the highest "average amortization of principal and interest". Basically, if you don't have any special request and you are not a large customer, usually you won't be able to do it. Allows you to choose to amortize the principal equally.

As for the misunderstanding that many people fall into, it is the "average repayment of principal and interest" that seems to be relatively small every month. They mistakenly believe that because the principal is reduced, the interest is also reduced. This will really harm others. Got it!

Only by choosing "average principal amortization" can you reduce the monthly repayment amount because the principal is reduced, and the interest is reduced along with it, but only at the beginning, you will pay more money!

# Real estate # Xinqing'an # Home loan # Interest # Loan # Bank # Principal # Principal and interest # Repayment # Pay off # Average # Payment # Underwriting # Down payment # Final payment # Deed tax # Performance fee # Settlement # Advantages # Disadvantages # Decreasing # Moonlight clan # Savings # Interest rate # Large amount # Misunderstanding # Stepping on thunder # Beheading # Leek # Choice

My balcony has great sunshine!

I will definitely go up there and sunbathe naked every day from now on🥰

This website does not have those annoying ads that block the webpage and hinder reading!

If you think the article I wrote is helpful to you, could you please fill in a Questionnaire, allowing me to better understand everyone’s needs and write more high-quality content.